𝐓𝐚𝐱 & 𝐒𝐮𝐩𝐞𝐫 𝐂𝐡𝐚𝐧𝐠𝐞𝐬 𝐂𝐨𝐦𝐢𝐧𝐠 𝐈𝐧 𝟐𝟎𝟐𝟔: 𝐀𝐓𝐎 𝐔𝐩𝐝𝐚𝐭𝐞𝐬 𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐞𝐝

𝐓𝐚𝐱 & 𝐒𝐮𝐩𝐞𝐫 𝐂𝐡𝐚𝐧𝐠𝐞𝐬 𝐂𝐨𝐦𝐢𝐧𝐠 𝐈𝐧 𝟐𝟎𝟐𝟔: 𝐀𝐓𝐎 𝐔𝐩𝐝𝐚𝐭𝐞𝐬 𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐞𝐝

The Australian Taxation Office (ATO) has released several important tax and superannuation updates affecting businesses, employers, trusts, property estates, and tax practitioners for 2026. These updates include changes to fuel tax credits, Payday Super obligations, family trust elections, inherited property exemptions, trust reporting rules, and company tax eligibility requirements.

Understanding these changes early can help businesses stay compliant, improve reporting accuracy, and avoid unnecessary penalties or administrative issues.

🚛 𝐅𝐮𝐞𝐥 𝐓𝐚𝐱 𝐂𝐫𝐞𝐝𝐢𝐭 𝐑𝐚𝐭𝐞 𝐂𝐡𝐚𝐧𝐠𝐞𝐬 𝐅𝐫𝐨𝐦 𝟏 𝐀𝐩𝐫𝐢𝐥 𝟐𝟎𝟐𝟔

The ATO has updated fuel tax credit rates following a temporary reduction in fuel excise.

From 1 April 2026 to 30 June 2026:

✔ The heavy vehicle road user charge will be reduced to zero

✔ Eligible businesses using fuel in heavy vehicles on public roads may claim fuel tax credits equal to the fuel excise duty paid

This temporary change is designed to support businesses facing increased transport and logistics costs.

Businesses operating in transport, freight, construction, agriculture, and logistics should review their fuel usage records carefully to ensure correct claims are made.

⛽ 𝐀𝐓𝐎 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐏𝐥𝐚𝐧𝐬 𝐅𝐨𝐫 𝐇𝐢𝐠𝐡 𝐅𝐮𝐞𝐥 𝐂𝐨𝐬𝐭𝐬

The ATO is offering targeted payment plan support to eligible businesses impacted by high fuel costs.

Applications are available until 30 June 2026.

𝐄𝐥𝐢𝐠𝐢𝐛𝐢𝐥𝐢𝐭𝐲 𝐂𝐫𝐢𝐭𝐞𝐫𝐢𝐚

Businesses must:

✔ Hold an active ABN

✔ Demonstrate fuel-related business cost increases

✔ Have difficulty paying tax debts because of fuel costs

✔ Keep tax lodgments up to date within 3 months of the plan commencement

𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐬 𝐎𝐟 𝐓𝐡𝐞 𝐏𝐥𝐚𝐧

✔ No upfront payment required

✔ 36 equal monthly instalments over 3 years

✔ General Interest Charge (GIC) remission may apply if payment obligations are met

Businesses in fuel-sensitive industries should assess eligibility before the deadline.

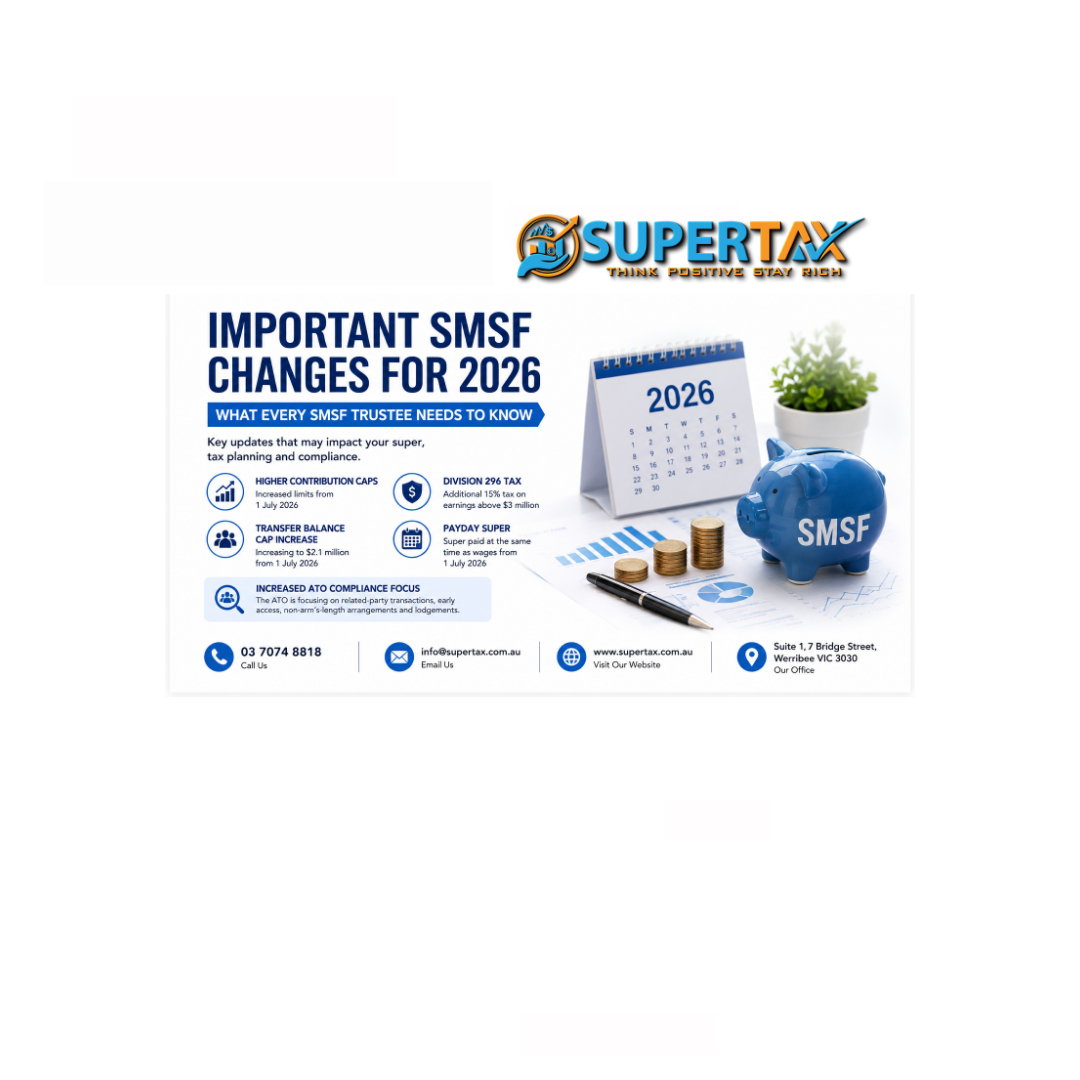

💰 𝐏𝐚𝐲𝐝𝐚𝐲 𝐒𝐮𝐩𝐞𝐫 𝐂𝐡𝐚𝐧𝐠𝐞𝐬 𝐅𝐫𝐨𝐦 𝟏 𝐉𝐮𝐥𝐲 𝟐𝟎𝟐𝟔

One of the most significant superannuation reforms coming in 2026 is Payday Super.

Under the new rules:

✔ Super contributions must generally reach employees’ super funds within 7 business days of payday

✔ Super funds will have 3 business days to allocate contributions or return unallocated amounts

✔ Employers must calculate contributions based on qualifying earnings (QE)

These reforms aim to improve super payment transparency and reduce unpaid super obligations.

📌 𝐒𝐮𝐩𝐞𝐫 𝐅𝐮𝐧𝐝 𝐒𝐭𝐚𝐩𝐥𝐢𝐧𝐠 𝐑𝐞𝐦𝐢𝐧𝐝𝐞𝐫

The ATO also reminded employers about stapled super fund obligations.

When onboarding employees:

✔ Employers must offer super fund choice

✔ If no choice is made, employers should request stapled super fund details from the ATO

✔ If a stapled fund exists, contributions should be paid to that fund

This process helps reduce unnecessary duplicate super accounts.

🏠 𝐈𝐧𝐡𝐞𝐫𝐢𝐭𝐞𝐝 𝐌𝐚𝐢𝐧 𝐑𝐞𝐬𝐢𝐝𝐞𝐧𝐜𝐞 – 𝟐 𝐘𝐞𝐚𝐫 𝐄𝐱𝐭𝐞𝐧𝐬𝐢𝐨𝐧𝐬

The ATO has updated guidance regarding the main residence exemption for inherited property.

𝐀𝐮𝐭𝐨𝐦𝐚𝐭𝐢𝐜 𝐄𝐱𝐭𝐞𝐧𝐬𝐢𝐨𝐧 (𝐔𝐩 𝐓𝐨 𝟏𝟖 𝐌𝐨𝐧𝐭𝐡𝐬)

An extension may apply if delays were caused by:

✔ Will disputes

✔ Legal ownership complications

✔ Estate administration issues

The property must generally:

✔ Be listed for sale promptly after issues are resolved

✔ Be actively marketed

✔ Be sold within 12 months of listing

The ATO has clarified that waiting for better market conditions or delaying action for convenience will not usually qualify.

Executors and beneficiaries should review approaching deadlines carefully.

👨👩👧 𝐅𝐚𝐦𝐢𝐥𝐲 𝐓𝐫𝐮𝐬𝐭 𝐄𝐥𝐞𝐜𝐭𝐢𝐨𝐧𝐬 – 𝐈𝐧𝐜𝐫𝐞𝐚𝐬𝐞𝐝 𝐕𝐢𝐬𝐢𝐛𝐢𝐥𝐢𝐭𝐲

The ATO has improved Online Services for Agents to make family trust elections easier to monitor.

Agents can now view:

✔ Election receipt dates

✔ Election types

✔ Revocation details

✔ Final applicable election years

This improves transparency and tracking of trust-related elections.

🏢 𝐁𝐚𝐬𝐞 𝐑𝐚𝐭𝐞 𝐄𝐧𝐭𝐢𝐭𝐲 (𝐁𝐑𝐄) 𝐂𝐨𝐦𝐦𝐨𝐧 𝐌𝐢𝐬𝐭𝐚𝐤𝐞𝐬

The ATO has identified ongoing errors in BRE eligibility reporting.

To qualify as a Base Rate Entity:

✔ Aggregated turnover must be below $50 million

✔ Passive income must not exceed 80% of assessable income

⚠️ Common Errors Include

❌ Excluding connected entity turnover

❌ Incorrect treatment of capital gains

❌ Overlooking passive income such as rent, royalties, dividends, or interest

❌ Failing to reassess eligibility annually

Companies should review BRE eligibility every year rather than assuming eligibility continues automatically.

📋 𝐌𝐨𝐝𝐞𝐫𝐧𝐢𝐬𝐚𝐭𝐢𝐨𝐧 𝐎𝐟 𝐓𝐚𝐱 𝐀𝐝𝐦𝐢𝐧𝐢𝐬𝐭𝐫𝐚𝐭𝐢𝐨𝐧 𝐒𝐲𝐬𝐭𝐞𝐦𝐬 (𝐌𝐓𝐀𝐒)

The ATO has also released guidance on upcoming trust reporting changes under the MTAS program from 1 July 2026.

𝐊𝐞𝐲 𝐂𝐡𝐚𝐧𝐠𝐞𝐬

✔ New trust tax return labels

✔ Improved pre-lodgment checks

✔ Simpler reporting requirements

✔ Expanded beneficiary pre-fill data

✔ Improved trust distribution reporting

From Tax Time 2027, additional changes are expected including:

✔ Expanded pre-fill reporting

✔ Improved family trust election reporting

✔ Simplified non-resident beneficiary reporting

✔ Online trust lodgment functionality

Trustees and practitioners should prepare early for these reporting changes.

📌 𝐖𝐡𝐚𝐭 𝐓𝐡𝐢𝐬 𝐌𝐞𝐚𝐧𝐬 𝐅𝐨𝐫 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬𝐞𝐬 & 𝐓𝐚𝐱𝐩𝐚𝐲𝐞𝐫𝐬

The 2026 regulatory updates show the ATO continuing to focus on:

✔ Better reporting accuracy

✔ Faster data matching

✔ Improved super compliance

✔ Stronger trust reporting systems

✔ Greater visibility across tax obligations

Businesses, employers, trustees, and investors should review their systems and processes now to avoid compliance issues later.

📞 𝗧𝗮𝗹𝗸 𝘁𝗼 𝗦𝘂𝗽𝗲𝗿𝘁𝗮𝘅 𝗧𝗼𝗱𝗮𝘆

Need help understanding how these 2026 tax and superannuation updates affect your business or investment structure?

The team at Supertax

can help you stay compliant and prepare for upcoming ATO changes.

🌐 https://supertax.com.au/

📍 Suite 1, 7 Bridge St, Werribee VIC 3030

📞 (03) 7074 8818

📧 info@supertax.com.au

⚠️ Disclaimer: General information only. This article does not constitute financial, legal, or tax advice. Please seek professional advice for your personal circumstances.

Other posts