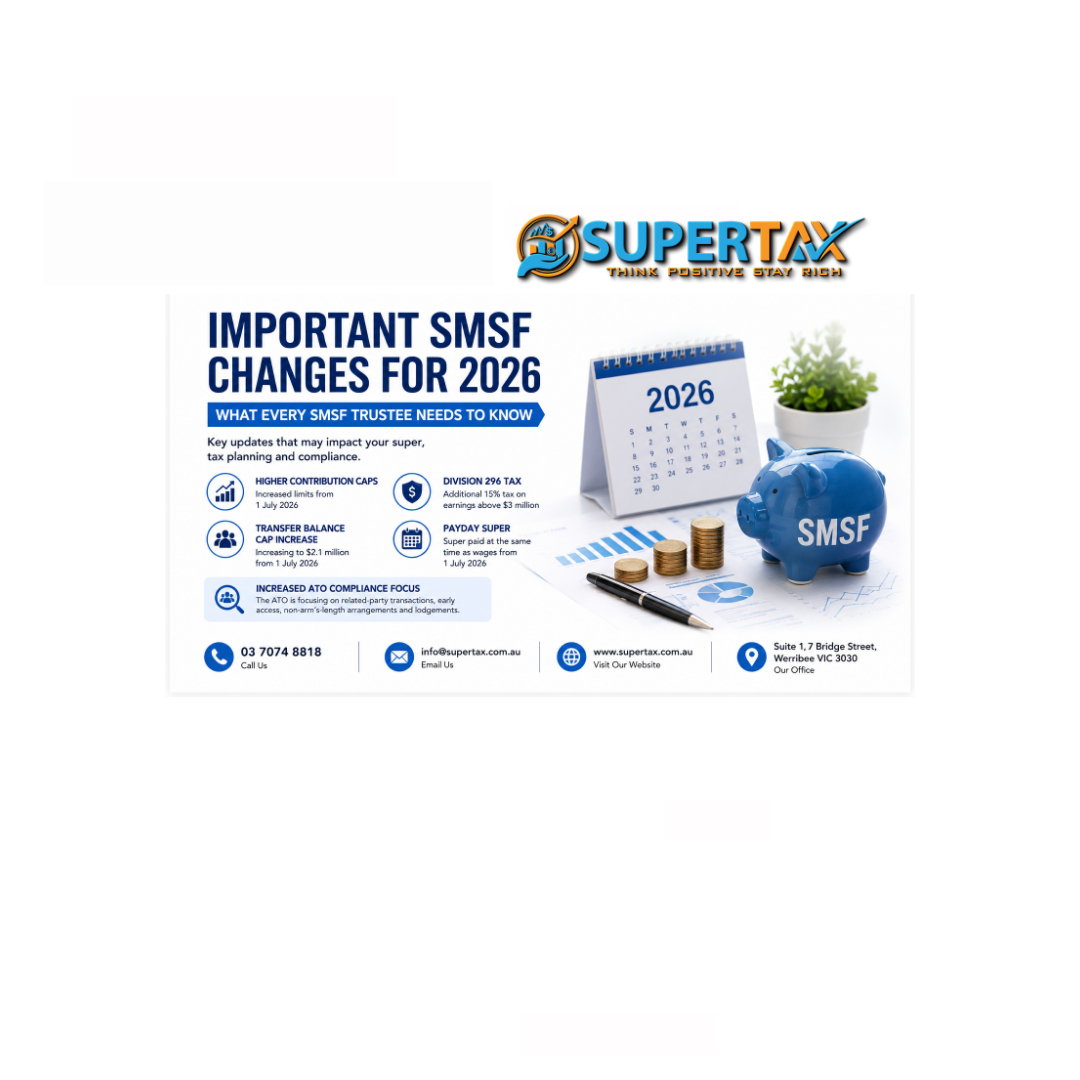

Australia Division 296 Tax vs Current Super Rules: Complete 2026 Guide

Australia Division 296 Tax vs Current Super Rules: Complete 2026 Guide

Introduction

The proposed Division 296 super tax is one of the most significant potential changes to Australia’s superannuation system in recent years.

Designed to target individuals with super balances exceeding $3 million, this reform has raised key concerns for SMSF members, business owners, and high-net-worth investors.

At Supertax, we believe clarity is essential. This guide provides a simple and factual comparison between the current super tax system and the proposed Division 296 rules—helping you make informed decisions about your retirement strategy.

Division 296 vs Current Super Rules (Quick Overview)

✅ Current System

- 15% tax on earnings (accumulation phase)

- 0% tax in pension phase

- Capital gains discount (effective 10% tax)

⚠️ Proposed Division 296

- Additional 15% tax on earnings above $3 million

- Effective tax rate of 30% on excess portion

- Includes unrealised (paper) gains

- Applies regardless of pension or accumulation phase

How Super Is Currently Taxed in Australia

Australia’s super system is designed to be tax-effective, encouraging long-term wealth creation.

Current Tax Treatment:

| Stage | Tax Rate |

|---|---|

| Concessional Contributions | 15% |

| Earnings (Accumulation Phase) | 15% |

| Capital Gains (>12 months) | 10% |

| Pension Phase Earnings | 0% |

👉 This concessional structure makes super one of the most powerful tools for retirement planning.

What Is Division 296?

Division 296 is a proposed additional tax on super earnings for individuals whose Total Super Balance (TSB) exceeds $3 million.

Key Features:

- Applies only to earnings on the excess balance

- Adds an extra 15% tax

- Includes unrealised gains

- Threshold is not indexed to inflation

👉 Over time, more Australians may be affected as balances grow.

Key Differences: Division 296 vs Current Rules

| Feature | Current System | Division 296 Proposal |

|---|---|---|

| Balance Threshold | No threshold | Applies above $3M |

| Earnings Tax | 15% | Up to 30% |

| Pension Phase | Tax-free | May still apply |

| Unrealised Gains | Not taxed | Taxed |

| Structure | Uniform | Tiered |

Who Will Be Affected?

The proposed tax is expected to impact around 80,000 Australians (≈0.5%) initially.

Likely affected groups:

- SMSF members with large balances

- Long-term investors

- Business owners & high-income professionals

- Property investors within super

Why Division 296 Is Controversial

1. Tax on Unrealised Gains

- Tax may apply on assets not yet sold

- Major shift from traditional tax rules

2. Liquidity Challenges

- SMSFs holding property may struggle to pay tax without selling assets

3. Investment Strategy Impact

- Could discourage long-term investment

- Changes risk-return calculations

Worked Example: $4 Million Super Balance

Scenario:

- Total Balance: $4M

- Annual Growth: 5% ($200,000)

Current System:

👉 Tax = 15% of $200,000 = $30,000

Division 296:

- Excess Balance = $1M

- Proportion = 25%

- Attributable Earnings = $50,000

- Additional Tax = $7,500

✅ Total Tax:

👉 $37,500 (Extra $7,500)

Strategies to Consider

At Supertax, we recommend proactive planning rather than reactive decisions.

Potential strategies:

- Review contribution strategies

- Consider investing outside super

- Reassess SMSF asset allocation

- Plan for liquidity needs

- Seek expert tax advice

Super Strategy Checklist

✔ Check total super balance

✔ Project future growth

✔ Review SMSF investments

✔ Monitor legislative updates

✔ Consult a qualified adviser

Common Misunderstandings

❌ “Tax applies to entire balance”

✔ Only applies to earnings above $3M

❌ “It’s a wealth tax”

✔ It is a tax on earnings

❌ “Pension phase avoids tax”

✔ Applies regardless of phase

❌ “Threshold increases with inflation”

✔ Not indexed

FAQs

What is Division 296?

A proposed 15% additional tax on earnings for super balances above $3 million.

Does it include unrealised gains?

Yes, which is one of the most debated aspects.

When will it start?

Proposed from 1 July 2025 (subject to legislation).

Who pays the tax?

The individual member, not the super fund.

What Should You Do Now?

The best approach is to stay informed and plan ahead.

✔ Avoid rushed decisions

✔ Review your financial position

✔ Seek professional advice

At Supertax, we help clients navigate complex tax changes with clarity and confidence.

Conclusion

Division 296 represents a major shift in how high-balance super accounts may be taxed.

While it affects a small group today, its long-term implications could be broader.

👉 Smart planning today can protect your future.

📞 Need Expert Advice?

Supertax

Your trusted partner for tax planning and compliance.

👉 Contact us today to review your super strategy and prepare for upcoming changes.

👉 Get expert support and peace of mind today.

📍 Suite 1, 7 Bridge St, Werribee Victoria 3030, Australia

📞 (03) 7074 8818

📧 info@supertax.com.au

🌐 https://supertax.com.au/

⚠️ Disclaimer

This article is for general information only and does not constitute financial or tax advice. Please consult a registered tax agent or licensed financial adviser before making decisions.

Other posts