Government Updates Impacting Tax, R&D Incentives and Superannuation (2026)

Government Updates Impacting Tax, R&D Incentives and Superannuation (2026)

Australian tax laws and financial regulations continue to evolve, creating new opportunities and compliance requirements for individuals, investors, and businesses. The latest government updates introduce important changes to superannuation taxation, R&D tax incentives, trust reporting, and tax expenditure policies.

Understanding these updates is essential for effective tax planning, compliance, and long-term financial strategy. Below is a detailed overview of the key changes impacting Australian taxpayers from 2025 onwards.

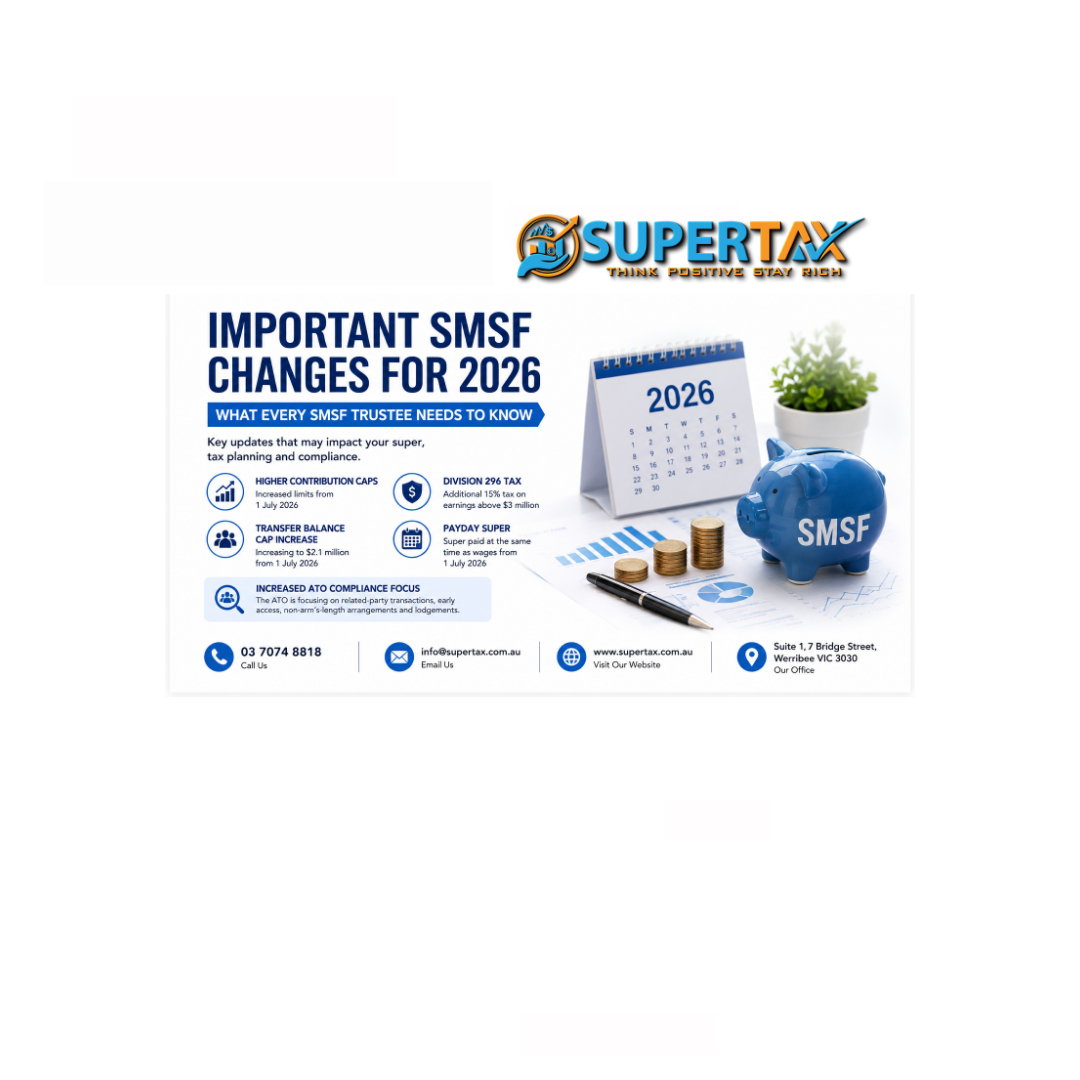

Division 296: New Tax on High Superannuation Balances

The Australian Government has released draft legislation for the Better Targeted Super Concessions measure, introducing a new tax known as Division 296.

This measure is designed to reduce tax concessions for individuals with superannuation balances exceeding $3 million.

Key Proposed Changes

From the 2026–27 income year, higher tax rates may apply:

- Up to 30% tax on earnings from balances between $3 million and $10 million

- Up to 40% tax on earnings from balances above $10 million

The Division 296 tax will be applied directly to individuals, separate from existing superannuation fund taxes.

Payment Options

Individuals will have flexibility in how they pay this tax:

- Withdraw funds from their superannuation account, or

- Pay using personal funds held outside of super

Threshold Indexation

The proposed thresholds of $3 million and $10 million will be indexed to CPI, ensuring they increase over time in line with inflation and remain aligned with the transfer balance cap framework.

Transitional Arrangements for Superannuation Assets

The draft legislation includes transitional rules for assets held before the new rules take effect.

Two methods are proposed for calculating Capital Gains Tax (CGT) adjustments:

- Cost base adjustment method – generally for small super funds

- Factor method – for other complying superannuation funds

A key rule applies for the 2026–27 income year:

Division 296 will be assessed based on your Total Superannuation Balance (TSB) as at 30 June 2027.

👉 If your balance is below $3 million at that date, you will not be subject to Division 296 tax for that year.

Further regulations are expected to clarify:

- Exclusions from superannuation earnings

- Attribution of earnings to super interests

- Valuation methods

- CGT transition calculations

2025–26 Tax Expenditures and Insights Statement

The government has released the 2025–26 Tax Expenditures and Insights Statement (TEIS), which highlights areas where tax concessions reduce government revenue.

This report provides insight into areas that may be targeted for future tax reforms.

Key Tax Expenditures Include:

- Main residence CGT exemption

- Concessional taxation of super contributions and earnings

- Rental property deductions

- CGT discount for individuals and trusts

- Work-related expense deductions

- Lower tax rates for small businesses

- Fringe Benefits Tax (FBT) exemptions

These areas are likely to remain under government scrutiny.

Changes to the R&D Tax Incentive

The government has proposed targeted exclusions from the Research and Development Tax Incentive (RDTI).

Proposed Exclusions

The following activities may no longer qualify:

- Tobacco-related research

- Gambling-related technologies

- Nicotine and vaping product development

These exclusions apply to both direct and supporting R&D activities.

Exception for Harm Reduction

An exception may apply where research is conducted solely to reduce harm associated with tobacco or nicotine use.

However, due to the strict “sole purpose” test, projects with mixed objectives may not qualify.

👉 These changes are expected to apply from 1 July 2025.

Businesses in technology, software, and innovation sectors should carefully review their R&D activities to ensure continued eligibility.

Modernising Trust Administration Systems

The government has proposed reforms under the Treasury Laws Amendment Bill 2025 to simplify trust reporting.

Key Changes to TFN Reporting

- Trustees will report beneficiary Tax File Numbers (TFNs) annually with the trust tax return

- Quarterly TFN reporting requirements will be removed

This applies where:

- The beneficiary has provided a TFN

- The beneficiary receives a share of trust income

Additional ATO Powers

The ATO may notify trustees if:

- A TFN is incorrect

- A TFN has been cancelled or withdrawn

- Information does not match records

These changes aim to:

- Improve data matching

- Enable pre-filled tax returns

- Ensure accurate tax reporting

👉 The new rules are expected to apply from 1 July 2026.

Transfer Balance Cap Increase

Following the December 2025 CPI release, the Transfer Balance Cap (TBC) will increase.

From 1 July 2026:

$2.0 million → $2.1 million

This change may create new opportunities for tax-effective retirement planning.

Retirement Income Stream Planning

Individuals starting a retirement-phase income stream after 1 July 2026 will benefit from the full $2.1 million cap.

👉 In some cases, delaying retirement income streams until this date may result in better tax outcomes.

Careful planning with an accountant is essential to maximise benefits.

Final Thoughts

The latest Australian government updates introduce major changes across:

- Superannuation taxation

- R&D tax incentives

- Trust administration

- Retirement planning

Staying informed helps individuals and businesses:

- Plan for upcoming tax changes

- Maintain compliance

- Identify strategic tax-saving opportunities

Working with a professional accountant ensures your financial strategy remains efficient, compliant, and future-ready.

Need Expert Tax Advice?

At Supertax, we provide expert guidance on:

- Superannuation tax planning

- R&D tax incentives

- Trust taxation

- Business and individual tax strategies

Our team helps you stay compliant while maximising your financial outcomes.

📞 Contact Supertax today to discuss how these updates impact your situation.

📍 Suite 1, 7 Bridge St, Werribee Victoria 3030, Australia

📞 (03) 7074 8818

📧 info@supertax.com.au

🌐 https://supertax.com.au/

Other posts