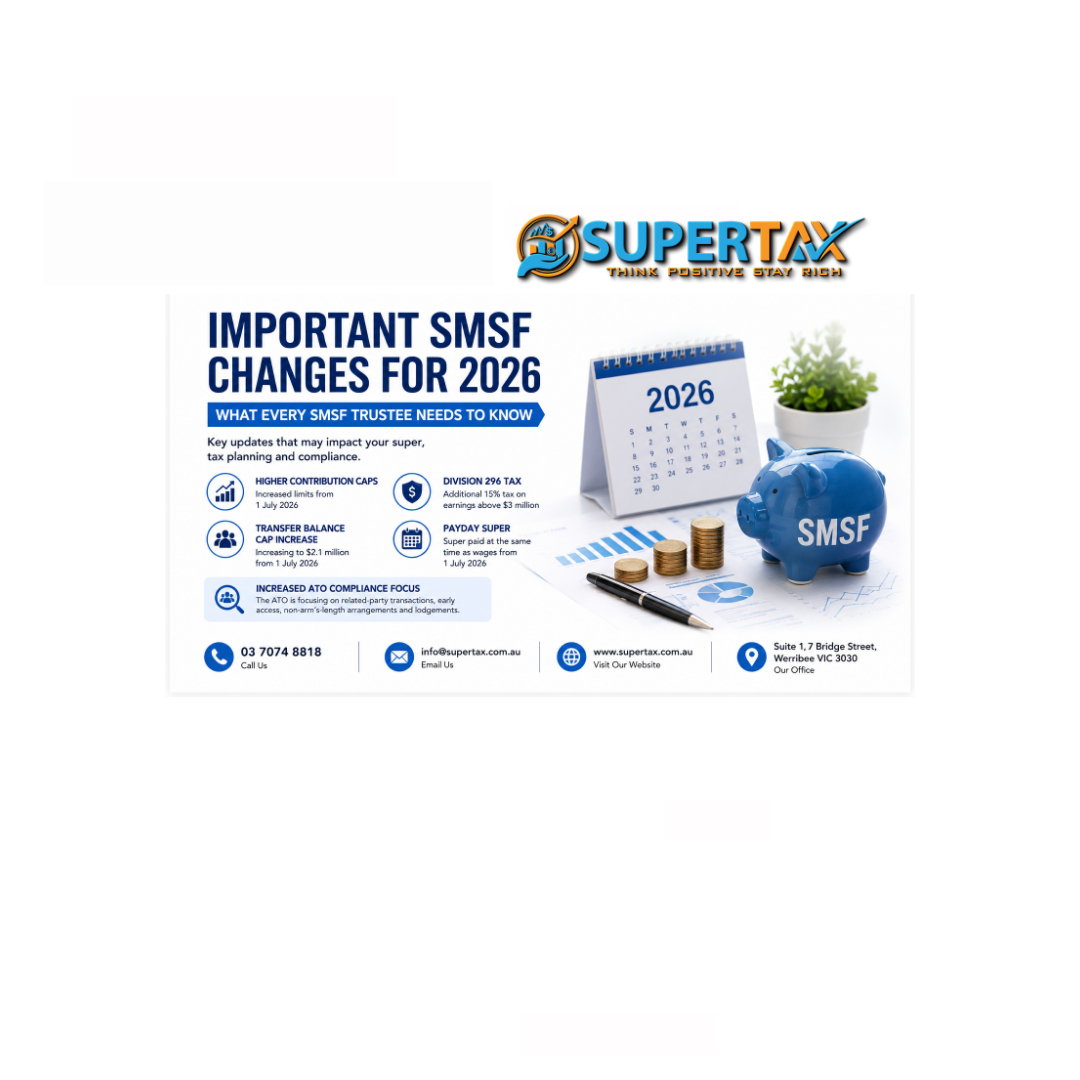

𝐓𝐡𝐞 𝐄𝐧𝐝 𝐎𝐟 𝐐𝐮𝐚𝐫𝐭𝐞𝐫𝐥𝐲 𝐒𝐮𝐩𝐞𝐫? 𝐏𝐚𝐲𝐝𝐚𝐲 𝐒𝐮𝐩𝐞𝐫 𝐑𝐮𝐥𝐞𝐬 𝟐𝟎𝟐𝟔 𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐞𝐝

𝐓𝐡𝐞 𝐄𝐧𝐝 𝐎𝐟 𝐐𝐮𝐚𝐫𝐭𝐞𝐫𝐥𝐲 𝐒𝐮𝐩𝐞𝐫? 𝐏𝐚𝐲𝐝𝐚𝐲 𝐒𝐮𝐩𝐞𝐫 𝐑𝐮𝐥𝐞𝐬 𝟐𝟎𝟐𝟔 𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐞𝐝

From 1 July 2026, Australian employers are expected to face one of the biggest superannuation compliance changes in years.

Under the proposed payday super reforms, superannuation will no longer sit quietly in the background until quarter-end. Employers will be required to pay super at the same time as wages, with contributions reaching employee super funds within a much tighter timeframe.

For many businesses, this is not just a payroll update.

It is a major operational and cash flow shift that affects:

- Payroll systems

- Super payment timing

- Staff cash flow planning

- Payroll approvals

- STP reporting

- Business cash reserves

- Internal compliance processes

Businesses still relying on quarter-end habits could face serious pressure once the new rules begin.

𝐖𝐡𝐚𝐭 𝐈𝐬 𝐏𝐚𝐲𝐝𝐚𝐲 𝐒𝐮𝐩𝐞𝐫?

Under the current system, employers generally pay super quarterly.

Many businesses process wages weekly or fortnightly but delay super payments until the quarterly due date.

From 1 July 2026, that structure changes.

Super contributions are expected to be paid much closer to payday itself.

📌 Practical Example

Current system:

- Wages paid weekly

- Super paid quarterly

New payday super system:

- Weekly wages = weekly super payments

- Fortnightly wages = fortnightly super payments

This removes the long-standing timing gap businesses have relied on for years.

𝐖𝐡𝐲 𝐓𝐡𝐢𝐬 𝐂𝐡𝐚𝐧𝐠𝐞 𝐌𝐚𝐭𝐭𝐞𝐫𝐬

Many small businesses have traditionally treated super like a future obligation rather than an immediate payroll expense.

That approach becomes much harder under payday super.

📌 The Biggest Business Impacts

🔹 Less cash flow flexibility

🔹 Faster compliance pressure

🔹 Increased payroll accuracy requirements

🔹 Greater ATO visibility through STP Phase 2

🔹 More pressure on payroll systems and approvals

🔹 Reduced room for delayed payments or corrections

For businesses already operating with tight margins, the change could expose weak payroll systems very quickly.

𝐓𝐡𝐞 𝐄𝐧𝐝 𝐎𝐟 𝐓𝐡𝐞 “𝐐𝐮𝐚𝐫𝐭𝐞𝐫𝐥𝐲 𝐁𝐮𝐟𝐟𝐞𝐫”

A common business habit looks like this:

Wages are paid today.

Super gets dealt with later.

That timing gap has acted like a short-term cash flow buffer for many employers.

From July 2026, that buffer largely disappears.

Businesses will need enough cash available during each payroll cycle to cover:

- Employee wages

- PAYG withholding

- Superannuation obligations

All at roughly the same time.

That creates a much tighter payroll funding cycle.

𝐎𝐓𝐄 𝐓𝐨 𝐐𝐄 — 𝐓𝐡𝐞 𝐇𝐢𝐝𝐝𝐞𝐧 𝐂𝐨𝐦𝐩𝐥𝐢𝐚𝐧𝐜𝐞 𝐑𝐢𝐬𝐤

One of the most overlooked parts of the reform is the expected shift from:

- Ordinary Time Earnings (OTE)

to - Qualifying Earnings (QE)

Many businesses think payday super is only about payment timing.

It is not.

The broader QE system may capture additional earnings categories that businesses previously handled differently under payroll.

📌 Potential Risk Areas

🔸 Overtime mapping

🔸 Bonuses

🔸 Salary sacrifice arrangements

🔸 Allowances

🔸 Director payments

🔸 Payroll category coding

This means businesses could:

- Pay super on time

- But still underpay super incorrectly

That is where hidden compliance risks begin.

𝐇𝐨𝐰 𝐒𝐓𝐏 𝐏𝐡𝐚𝐬𝐞 𝟐 𝐂𝐡𝐚𝐧𝐠𝐞𝐬 𝐓𝐡𝐞 𝐑𝐢𝐬𝐤

Single Touch Payroll Phase 2 already gives the ATO far greater visibility over payroll reporting.

Once payday super begins, the ATO is expected to see:

- What payroll was reported

- What super should have been paid

- Whether payment timing aligns correctly

That means businesses may have less time to detect and correct payroll mistakes.

Late super payments may become visible much faster than before.

𝐊𝐞𝐲 𝐃𝐚𝐭𝐞𝐬 𝐅𝐨𝐫 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐎𝐰𝐧𝐞𝐫𝐬

📅 Important Transition Dates

🔹 March 2026 Quarter

Due: 28 April 2026

Current quarterly rules still apply.

🔹 June 2026 Quarter

Due: 28 July 2026

Expected to be the final quarter under the old system.

🔹 From 1 July 2026

Payday super rules are expected to apply.

Businesses should confirm final implementation details directly with current ATO and Treasury guidance before rollout.

𝐖𝐡𝐨 𝐖𝐢𝐥𝐥 𝐁𝐞 𝐌𝐨𝐬𝐭 𝐀𝐟𝐟𝐞𝐜𝐭𝐞𝐝?

The businesses likely to feel the biggest pressure are:

📌 Small Businesses Using Manual Processes

🔹 Manual payroll approvals

🔹 Spreadsheet-based tracking

🔹 Delayed reconciliations

🔹 Older payroll workflows

🔹 Tight weekly cash flow management

These businesses may struggle most with:

- Timing

- Accuracy

- Payroll discipline

- Funding pressure

𝐒𝐌𝐒𝐅 𝐓𝐫𝐮𝐬𝐭𝐞𝐞𝐬 𝐀𝐧𝐝 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐎𝐰𝐧𝐞𝐫𝐬 𝐍𝐞𝐞𝐝 𝐓𝐨 𝐏𝐚𝐲 𝐀𝐭𝐭𝐞𝐧𝐭𝐢𝐨𝐧

Business owners using:

- SMSFs

- Salary sacrifice strategies

- Personal deductible contributions

may need to monitor contribution timing much more carefully.

More frequent super contributions may:

- Affect contribution caps earlier

- Change cash flow timing

- Impact tax planning strategies

Contribution records and payment dates will become far more important.

𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐈𝐦𝐩𝐚𝐜𝐭 𝐅𝐨𝐫 𝐄𝐦𝐩𝐥𝐨𝐲𝐞𝐫𝐬

Many businesses focus only on the total super cost.

But the real issue is often timing.

📌 Example

Under the old system:

- Super may stay inside the business account for weeks

Under payday super:

- Super leaves the account much faster

That means:

🔸 Less working capital flexibility

🔸 Tighter bank balances

🔸 More pressure on payroll funding

🔸 Less ability to delay liabilities

Businesses with weak cash reserves may feel the impact immediately.

𝐂𝐨𝐦𝐦𝐨𝐧 𝐌𝐢𝐬𝐭𝐚𝐤𝐞𝐬 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬𝐞𝐬 𝐒𝐡𝐨𝐮𝐥𝐝 𝐀𝐯𝐨𝐢𝐝

🚫 Common Transition Risks

🔸 Treating super as a later finance task

🔸 Assuming old payroll mappings still work

🔸 Delaying software reviews until 2026

🔸 Relying on manual payroll approvals

🔸 Ignoring failed or rejected super payments

🔸 Running payroll with no cash flow buffer

Most compliance failures are expected to come from process weaknesses — not deliberate avoidance.

𝐏𝐫𝐚𝐜𝐭𝐢𝐜𝐚𝐥 𝐏𝐫𝐞𝐩𝐚𝐫𝐚𝐭𝐢𝐨𝐧 𝐂𝐡𝐞𝐜𝐤𝐥𝐢𝐬𝐭

Businesses should begin preparing well before July 2026.

📌 Recommended Actions

🔹 Review payroll software setup

🔹 Audit payroll categories and pay items

🔹 Test STP Phase 2 reporting accuracy

🔹 Review cash flow forecasting

🔹 Check super clearing house timing

🔹 Build stronger payroll approval systems

🔹 Verify employee fund details early

🔹 Create internal payroll exception processes

The earlier businesses review their systems, the easier the transition will be.

𝐅𝐢𝐧𝐚𝐥 𝐓𝐡𝐨𝐮𝐠𝐡𝐭𝐬

Payday super is more than a simple compliance update.

It changes:

- Payroll timing

- Cash flow management

- Super processing

- Internal payroll discipline

- Employer compliance risk

Businesses that prepare early will likely handle the transition far more smoothly.

Businesses that continue relying on old quarterly habits may face operational stress, late payment risks, and payroll problems very quickly once the new system begins.

The smartest approach is to treat payday super as:

👉 a payroll system review

👉 a cash flow planning exercise

👉 and a compliance risk project all at the same time.

📞 𝗧𝗮𝗹𝗸 𝘁𝗼 𝗦𝘂𝗽𝗲𝗿𝘁𝗮𝘅 𝗧𝗼𝗱𝗮𝘆

🌐 Supertax

📍 Suite 1, 7 Bridge St, Werribee VIC 3030

📞 (03) 7074 8818

📧 info@supertax.com.au

Other posts