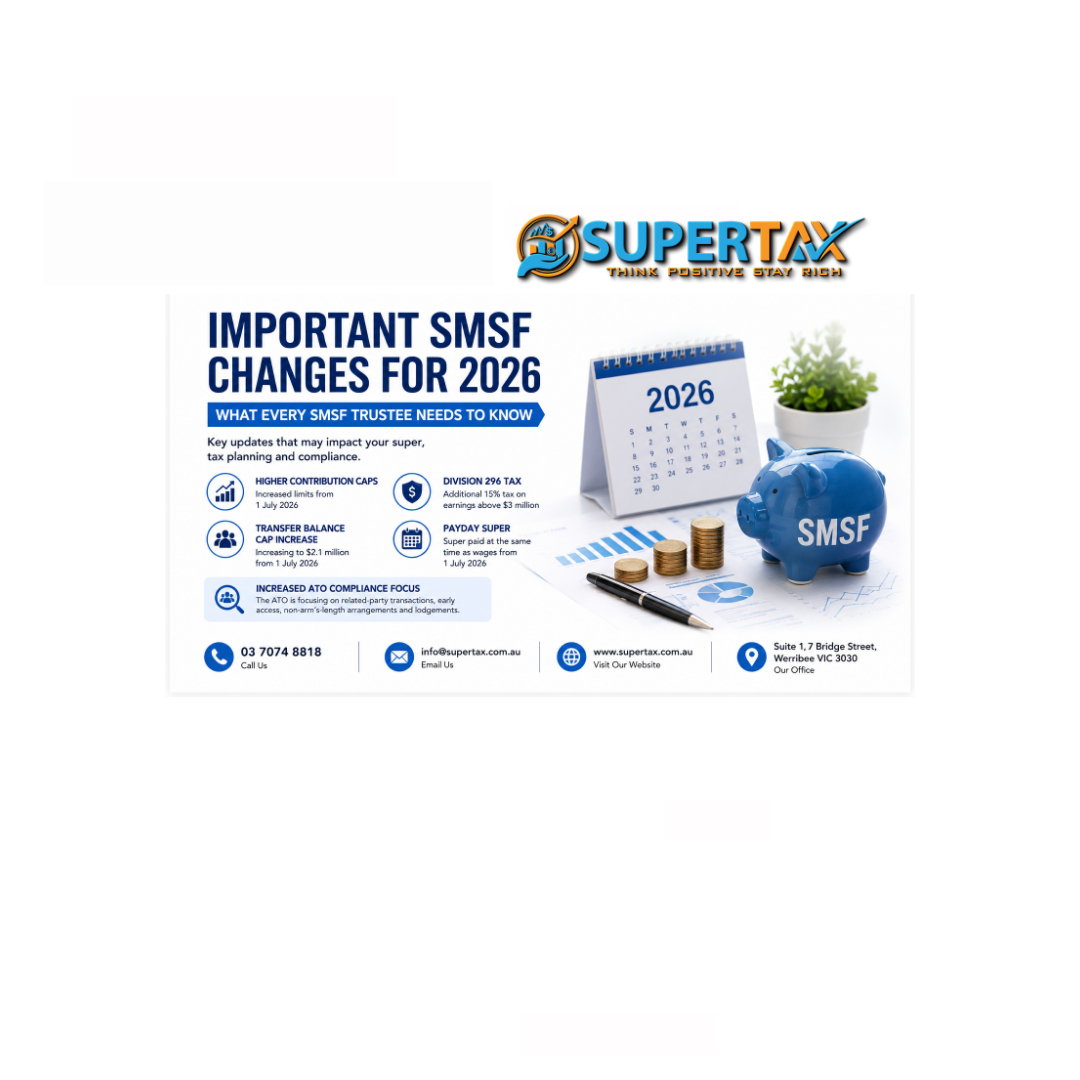

Important SMSF Changes for 2026 What Every Australian SMSF Trustee Needs to Know

Australia’s superannuation landscape continues to evolve, and 2026 is shaping up to be one of the most significant years for Self-Managed Super Funds (SMSFs). With proposed changes including the introduction of Division 296 tax, increased contribution caps, a higher transfer balance cap, and the implementation of Payday Super, SMSF trustees need to understand how these developments may affect their retirement strategies and compliance obligations.

In this article, we examine the key SMSF changes for 2026 and explain what trustees should do now to prepare.

Understanding SMSFs in Today’s Environment

A Self-Managed Super Fund (SMSF) provides Australians with greater control over their retirement savings and investment decisions. However, with this flexibility comes increased responsibility. Trustees are required to comply with superannuation laws, maintain appropriate records, implement investment strategies, and ensure the fund operates solely for retirement purposes.

As regulatory scrutiny increases and superannuation reforms continue, staying informed has never been more important.

Division 296 Tax: Additional Tax for High-Balance Super Accounts

One of the most widely discussed superannuation reforms is the proposed Division 296 tax.

Under the proposed legislation, individuals with total superannuation balances exceeding $3 million may be subject to an additional 15% tax on earnings attributable to the portion of their balance above the $3 million threshold.

Who Will Be Affected?

The measure primarily targets high-net-worth individuals with substantial superannuation balances. While relatively few Australians currently hold more than $3 million in super, many SMSF members who own commercial properties, large share portfolios, or other appreciating assets could potentially be impacted in the future.

Why SMSF Trustees Should Pay Attention

SMSFs often hold assets that may increase significantly in value over time. Trustees should consider:

- Reviewing long-term retirement strategies.

- Assessing future balance projections.

- Considering pension strategies and withdrawal plans.

- Obtaining professional advice regarding tax implications.

Early planning may help minimise future tax liabilities and provide greater flexibility.

Transfer Balance Cap Increasing to $2.1 Million

The General Transfer Balance Cap is expected to increase from $2.0 million to $2.1 million from 1 July 2026.

The Transfer Balance Cap limits the amount of superannuation that can be transferred into the tax-free retirement phase.

Why This Matters

The increase allows retirees to move an additional $100,000 into a retirement pension account where investment earnings are generally tax-free.

Potential benefits include:

- Increased tax-free income in retirement.

- Greater flexibility for retirement planning.

- Improved pension structuring opportunities.

- Enhanced tax efficiency for SMSF members approaching retirement.

Trustees nearing retirement should review their pension commencement strategies before making major decisions.

Higher Contribution Caps Expected from 1 July 2026

Contribution caps are expected to increase due to indexation.

Expected New Contribution Limits

Expected New Contribution Limits

| Contribution Type | Current Cap | Expected New Cap |

|---|---|---|

| Concessional Contributions | $30,000 | $32,500 |

| Non-Concessional Contributions | $120,000 | $130,000 |

| Bring-Forward Rule | $360,000 | $390,000 |

Higher contribution caps provide valuable opportunities to:

- Increase retirement savings.

- Reduce taxable income through concessional contributions.

- Boost super balances before retirement.

- Implement wealth transfer strategies.

Individuals considering large contributions should seek advice to ensure they remain within allowable limits and avoid excess contribution penalties.

Payday Super: A Significant Change for Employers and Employees

The Federal Government is introducing Payday Super from 1 July 2026.

Currently, employers generally pay Superannuation Guarantee (SG) contributions quarterly. Under the new system, super contributions will need to be paid much closer to payday.

Benefits of Payday Super

The new system aims to:

- Improve retirement outcomes for employees.

- Reduce unpaid superannuation.

- Increase transparency.

- Ensure super contributions are received sooner.

Impact on SMSFs

For SMSF members receiving employer contributions directly into their SMSF, contributions may arrive more regularly throughout the year.

Trustees should ensure their SMSF bank accounts and administration processes are capable of handling more frequent transactions.

Increased ATO Compliance and Regulatory Focus

The Australian Taxation Office (ATO) continues to increase its focus on SMSF compliance.

Trustees should expect ongoing scrutiny in areas including:

Related-Party Transactions

All transactions involving related parties must be conducted on arm’s-length terms and supported by proper documentation.

Non-Arm’s-Length Income (NALI)

The ATO continues to monitor arrangements that provide SMSFs with benefits unavailable to unrelated parties.

Illegal Early Release of Super

Accessing superannuation benefits before meeting a condition of release can result in significant penalties.

Late Lodgements

Trustees who fail to lodge annual returns on time may face:

- Administrative penalties.

- Auditor contravention reports.

- Loss of SMSF tax concessions.

- Possible fund disqualification.

Maintaining proper records and obtaining professional assistance can help trustees remain compliant.

Carry-Forward Concessional Contributions Still Available

Many SMSF members are unaware they can utilise unused concessional contribution caps from previous years.

Eligible members with a Total Super Balance below the applicable threshold may be able to make additional tax-deductible contributions using unused cap amounts accumulated over the previous five financial years.

This strategy can be particularly valuable for:

- Business owners.

- High-income earners.

- Individuals receiving capital gains.

- Those nearing retirement.

Downsizer Contributions Continue to Provide Opportunities

Australians aged 55 and over may be eligible to contribute up to $300,000 from the sale of their principal residence into superannuation.

For couples, this can provide an opportunity to contribute up to $600,000.

Benefits may include:

- Increasing retirement savings.

- Reducing personal taxable investment income.

- Enhancing estate planning strategies.

- Improving retirement cash flow.

What SMSF Trustees Should Do Now

To prepare for these changes, trustees should consider:

Review Your SMSF Strategy

Ensure your investment strategy remains appropriate and reflects current legislation.

Assess Contribution Opportunities

Take advantage of available contribution caps and tax-effective strategies.

Monitor Total Superannuation Balances

Members approaching the $3 million threshold should consider obtaining professional advice regarding future Division 296 implications.

Maintain Compliance

Keep records up to date, complete annual audits, and lodge SMSF returns on time.

Seek Professional Advice

The complexity of superannuation law continues to increase. Professional guidance can help trustees maximise opportunities while remaining compliant.

Conclusion

The SMSF sector is entering a period of significant change. From Division 296 tax and increased contribution caps to Payday Super and enhanced ATO compliance activity, trustees need to remain proactive and informed.

Understanding these developments and taking action early can help protect your retirement savings, improve tax outcomes, and ensure ongoing compliance.

At SuperTax, we assist SMSF trustees with tax compliance, annual accounts, audits, pension strategies, contribution planning, and ongoing SMSF administration.

Contact SuperTax

📞 Phone: 03 7074 8818

📧 Email: info@supertax.com.au

🌐 Website: www.supertax.com.au

📍 Address: Suite 1, 7 Bridge Street, Werribee VIC 3030

Our experienced SMSF specialists can help you navigate the latest superannuation changes and keep your fund compliant and tax-effective.

Disclaimer: This information is general in nature and does not constitute financial, taxation, or legal advice. Individual circumstances vary, and professional advice should be obtained before acting on this information.

Other posts